RDTI Reforms: The Numbers Behind Eligibility and Refund Losses

Alex Simmons - Co-Founder & CEO, Kashcade

With a background in big-bank product strategy at CommBank and management consulting at Accenture, Alex now works directly with Australian founders to unlock R&D funding at speed.

Patrick Nappa - Co-Founder & CTO, Kashcade

The data analysis and numbers in this piece were produced by Patrick Nappa, Co-Founder & CTO of Kashcade, a former Apple software engineer, University Medallist from the University of Sydney, and Forbes 30 Under 30 Asia honouree (Finance & Venture Capital).

On 12 May 2026, as part of the 2026-27 Federal Budget, the government announced seven changes to the RDTI - effective 1 July 2028.

The stated objectives are straightforward: better incentivise R&D spending that generates real economic spillovers and moderate the program's growing fiscal cost. A cost which has grown 70% in just 5 years from 2.6B in 2019-20 to 4.4B in 2023-24, and apparently driven largely by growth in claims for supporting activities and increased payments under the refundable offset.

There's been plenty of commentary since the announcement, and I’ve spoken to many advisors, and others in the community about their thoughts on the changes, but one thing that's been notably absent from the public conversation is hard numbers. How many businesses will lose eligibility entirely? How many will see their cash refund reduced - or disappear? And what does that mean for the advisors and other service providers whose practices are built around supporting them?

We went looking for those numbers.

For the purpose of this article, I’ve focused on the first 2, as data is available to glean some insight.

Reform 1: Raising the minimum expenditure floor from $20k to $50k

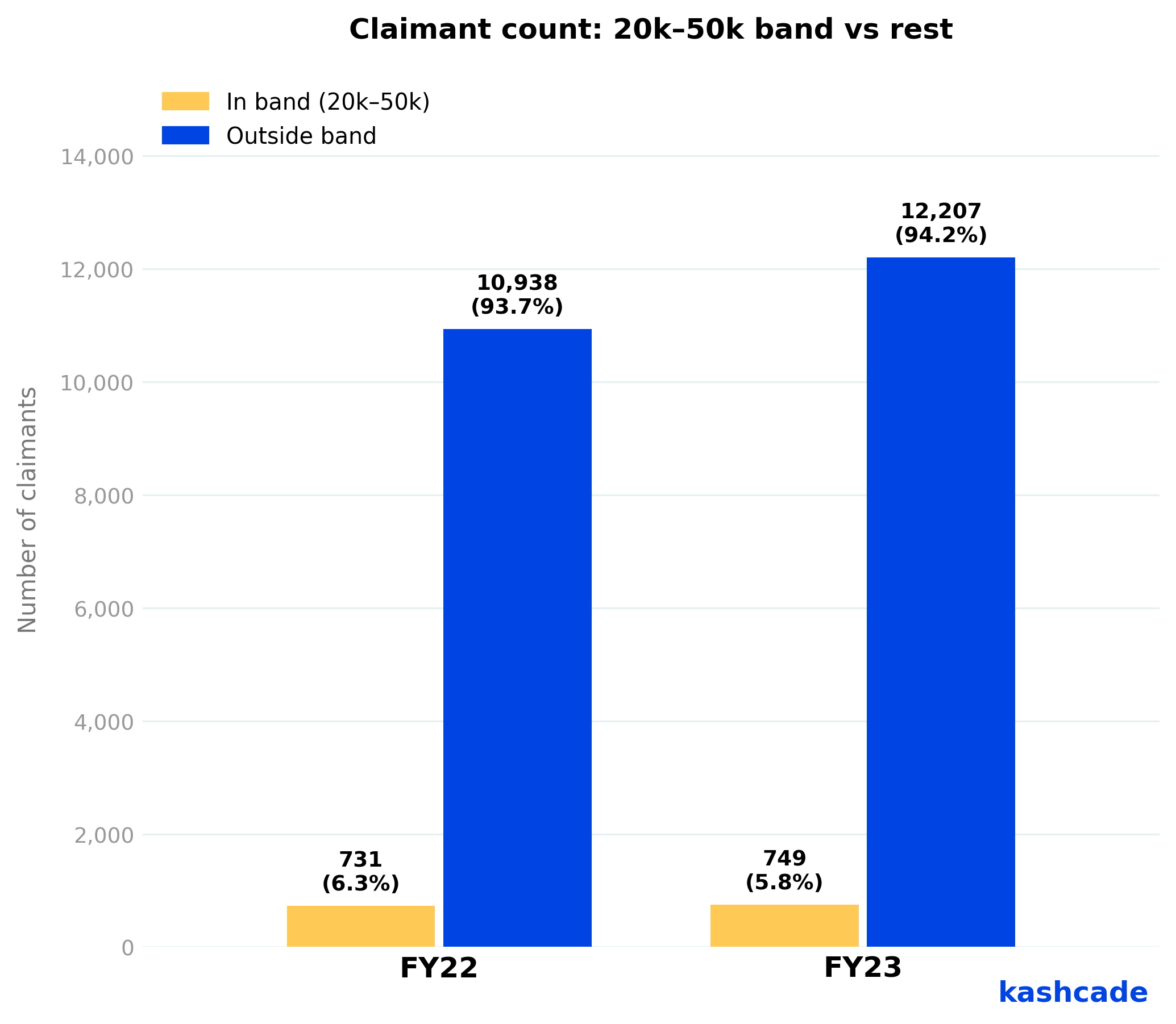

Almost 6% of the FY23 programs cohort will be ineligible with this change.

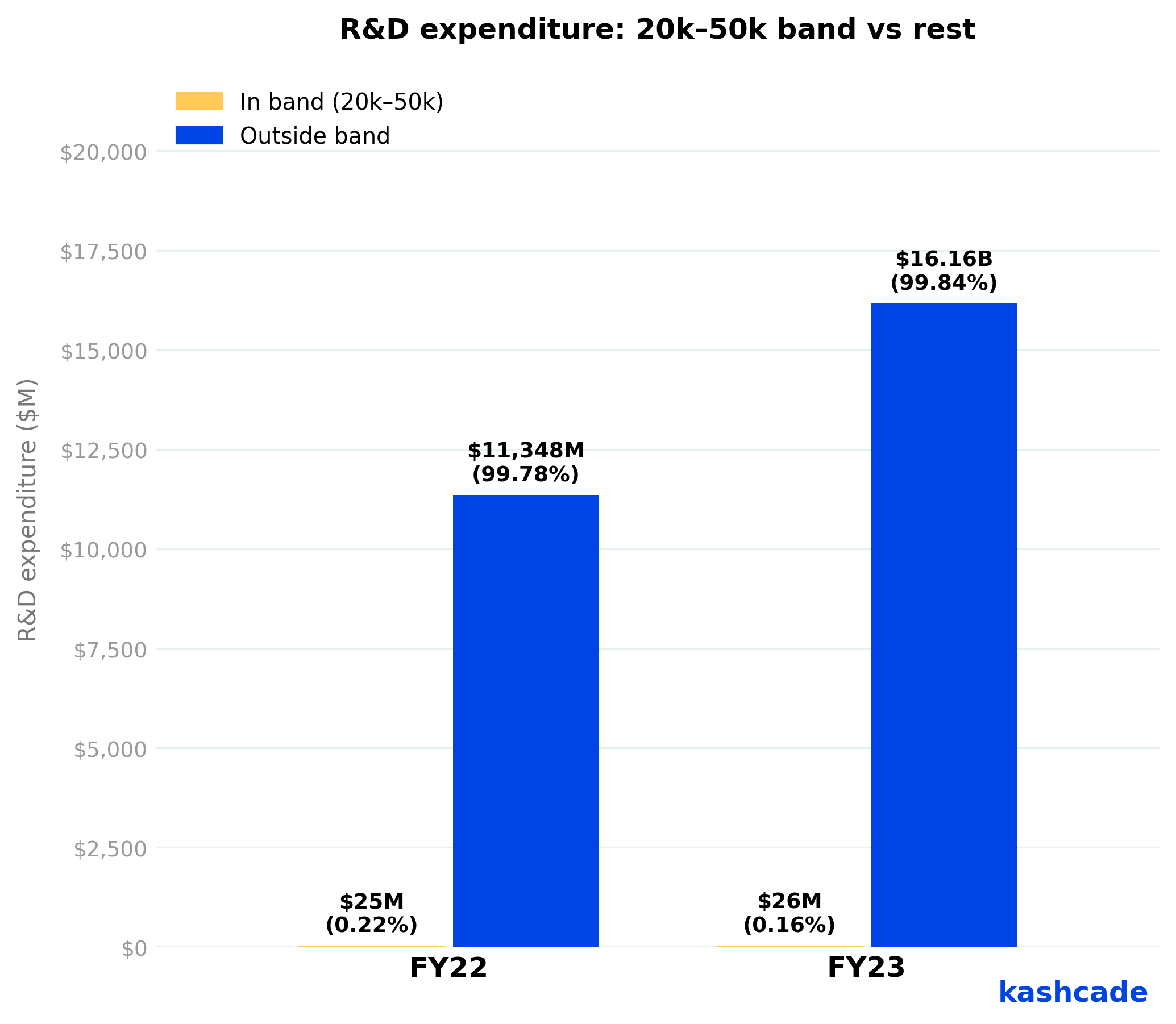

In FY23, 749 companies claimed between $20k and $50k in R&D expenditure. That's 5.8% of the total cohort of 12,956 companies. Their combined expenditure of $26M represents just 0.2% of the program's $16.2B total expenditure recorded. And assuming the overwhelming majority of these claimants are eligible to claim a 43.5% refundable offset, that would be ~$11.3M in refundable tax offsets of the total $2.54B paid out in FY23 – equivalent to 0.44%

One exception to flag: R&D activities undertaken with a Research Service Provider or Cooperative Research Centre remain eligible regardless of whether spend falls below $50K.

The immediate impact on advisor client bases of cutting this small segment looks minor. However, the pipeline impact for advisors is a different story and the FY22 cohort data shows why.

Here’s what happened to the equivalent cohort the year prior.

Of the 731 companies that claimed in the $20k–$50k band in FY22:

- 32% graduated to higher expenditure bands by FY23: 16% moved into the $50k–$100k band, 15% into $100k–$500k, and 1% into the $500k+ bracket

- The median claim for those who did return grew 50% ($17k increase), with a mean increase of 200%

- Total cohort expenditure grew from $25M in FY22 to $43M in FY23 - a 70% increase, despite the 40% attrition

This is what makes the $50k floor interesting. The companies in this band are often at the start of their R&D journey. A meaningful portion are on a fast growth trajectory, with over 30% of FY22 claimants moving into a higher band in FY23 as their R&D program has been able to grow with the support of the cash refund.

For advisors: The $50k threshold doesn't just eliminate 749 companies, it starts to erode the advisory pipeline. This gateway cohort is terminated from the advisory relationship before it has a chance to be meaningful.

Change 2: Restricting refundable offsets to the first 10 years of operation

This one is harder to read cleanly on how many of the current >10yr participants will actually be impacted. But here is what our analysis of the data told us:

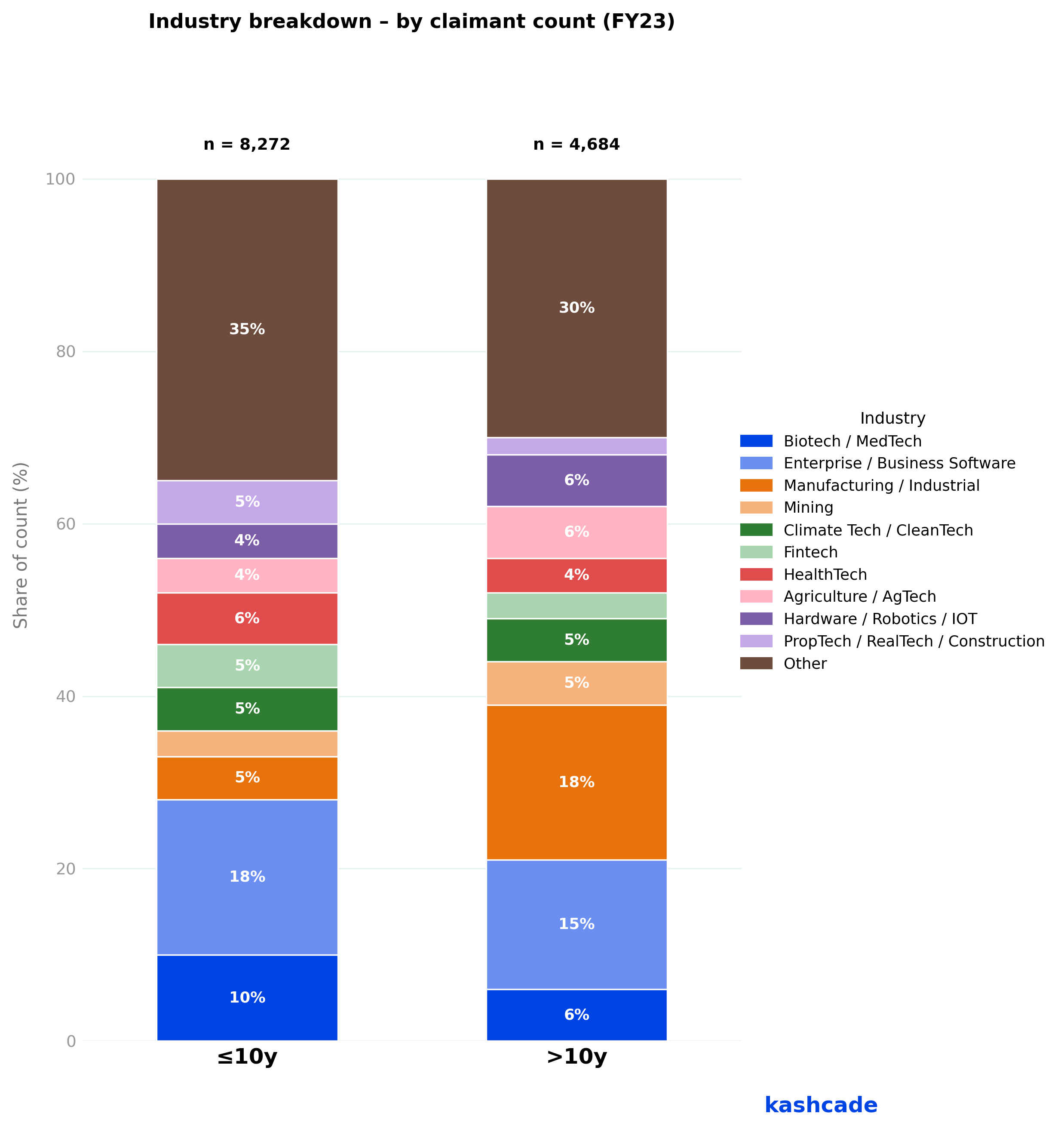

In FY23, 36% of RDTI claimants (4,684 companies) had been operating for more than 10 years. Their combined R&D expenditure was $8.5B - 52% of the program's total. More than half.

However, this doesn’t suddenly mean 36% of the program’s participants will go from a refundable offset to the non-refundable one. Many of these companies were already in the non-refundable bracket due to their level of turnover.

I want to be careful here. We don't know with certainty what proportion of that 36% are currently refundable as we don’t have access to revenue data of private companies and can’t verify how many would already be over the current >20M threshold. But even on a conservative read, a material number of companies will move from receiving a cash refund to receiving a tax offset. That's a real cashflow shift for many of these companies.

For advisors: Your customers currently eligible for a refund who fall into the non-refundable bracket under the new rules will feel a cashflow pinch as a result. Less cash returned means less capital available for reinvestment in R&D, and a possible reduction in the size of R&D programs as a result. Moreover, many investors we speak to are actually more willing to invest in a company they believe will get a cash refund from their R&D activities, as it means each dollar invested will go further and the company will have a better chance of being successful. Once again, this meas less capital might be availble for these companies.

One direct perspective from a client who'll be affected:

"The prospect of no longer being eligible after 10 years - which is now only 3 years away for us - is incredibly frustrating. While we could operate profitably without the program, it would materially reduce our ability to invest in innovation and growth." - Kiel Van Daal, Founder, Roilti

On the industry breakdown for >10 yr claimaints, the impact concentrates in a few places:

- Biotech and medtech carries the largest expenditure risk - 15% of the at-risk R&D spend - despite representing only 6% of >10 year claimants. These tend to be capital-intensive companies with longer development cycles, for whom the refundable offset is a major working capital tool.

- Manufacturing and industrial is most affected by participant count - 17% of >10 year claimants - and carries 11% of the at-risk expenditure.

- Enterprise and Business Software contributes 15% of participants and 9% by expenditure.

- Mining accounts for 8% of at-risk expenditure, and 4% of participants.

For advisors with clients in any of these industries who are approaching or past the 10-year mark: the cashflow impact is worth modelling now, not in 2028. Less cash returned means less capital available for reinvestment in R&D.

On the flip side, in the under-10yr cohort, two industries stand out as the largest claimants in R&D expenditure:

- Biotech and medtech: 17% of expenditure and 10% of participants

- Enterprise/Business Software: 14% of expenditure, 18% of participants

This is worth noting, as companies under 10 years old stand to benefit from two changes landing at once: the turnover threshold for the refundable offset rises from $20M to $50M, and the offset rate on core R&D activities increasing by 4.5 percentage points.

For Advisors: It’s worth mentioning to those in your team focused on new business acquisition: Biotech/Medtech and Enterprise/Business Software verticals deserve prioritising marketing and sales activities around, as they’re set to become even more cash endowed, and larger investment in R&D may follow.

If you're not already across the AusBiotech AusMedtech conference, it's worth getting on the calendar for next year.

What to do with this, practically

There’s a few things worth taking action on now:

Segment your client base by company age. Identify clients approaching the 10-year mark. Understand which of them currently access the refundable offset and have a conversation with them about how the proposed changes will impact their future RDTI claims once they come into effect and they’re no longer in the refundable segment.

Look closely at your sub-$50k clients. If you have clients who currently sit just below the new threshold, it's worth understanding whether their programs are on a growth trajectory - and whether there's a case for them to consolidate or expand their R&D activity to cross the new minimum in a way that makes sense for the business.

Start to think seriously about customer retention strategies. The changes announced are designed to better incentivise higher potential participants at the cost of providing support to lower potential participants. This likely means fewer participants receiving cash support, but for a segment of high potential participants (<10 yrs + >50K of R&D expenditure + annual turnover of up to 50M), there is potentially more cash on the table.

If you have clients in this segment, thinking about how best you can support and hold on to those clients will help balance or improve the losses you may experience from the segment of your clients who are no longer eligible for the RDTI or spend less on R&D as a result of moving to a non-refundable bracket.

Consider focusing new client acquisition on the verticals most likely to grow their R&D programs

In FY23, Biotech/medtech and Enterprise/Business software verticals collectively made up 31% of total expenditure and 28% of participants in the under-10-year cohort.

With companies under 10 years old set to benefit from two changes landing at once: the turnover threshold for the refundable offset rising from $20M to $50M, and the offset rate on core R&D activities increasing by 4.5 percentage points, the 2 verticals previously mentioned are likely to have more cash available, and their R&D programs could grow as a result.

For advisors focused on new client acquisition, this is where the addressable market may be largest and momentum in R&D strongest. If you're allocating BD effort in the next 12-18 months, these two verticals are worth prioritising.

Final words

These changes are not yet law. The consultation window matters, and the advisor community's collective read on what's workable and what isn't - is exactly the input that should be feeding into that process. If you have views on how these changes would affect your clients in practice, I'd encourage you to put them on record through a collective and orgainsed forum like the R&D Tax Advisors Association (RDTAA).

And if you'd like to talk through how any of this applies to a specific client scenario, feel free to reach out.